Credit Risk MachineLearning

Credit Risk MachineLearning (CML) system enables a credit modelling process with maximum precision, integrity, efficiency, user-friendliness and governance by the use of cutting-edge methodologies (Artificial Intelligence) and technology. These technologies and methodologies are made available to your organisation in a plug and play exercise without major implementation effort.

Credit Risk MachineLearning system enables your team to develop ‘best-in-class’ credit risk modelling:

- Credit Risk MachineLearning permits to create all Credit Risk models: credit rating, credit scoring, PD, LGD, EAD, CCF and others, for IRB and internal credit risk modelling

- No programming skills required: user-friendly interface and integrated dataflows completely eliminates need for coding when performing credit risk modelling; self-explanatory interface honed for credit risk modelling; re-do and un-do functions (similar to MS Office) applied to credit risk modelling functions

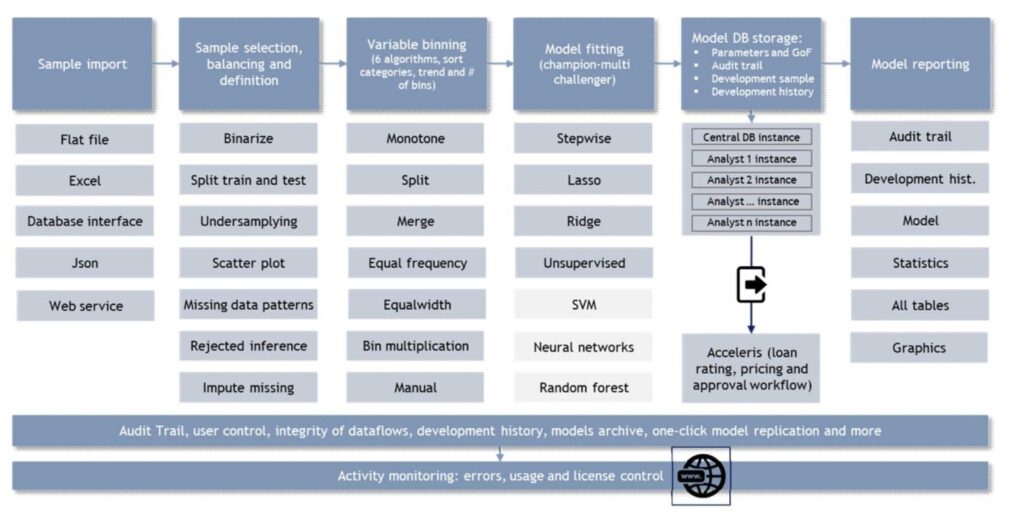

- Credit Risk MachineLearning system provides maximal prediction accuracy in credit risk modelling (credit rating, credit scoring, etc.); Champion-Multi challenger fitting method for credit rating, credit scoring and other credit risk models; simultaneous fitting and ranking of all credit risk models (under any GoF metric) to identify the most predictive credit rating, credit score and other credit risk models; AI applied to credit risk model fitting, feature binning, sample selection, best fit credit risk model identification and more; exhaustive coverage of credit risk modelling methods and ‘goodness- of-fit’ metrics.

- Credit Risk MachineLearning system has strong model governance in credit risk modelling: Full audit trail of all modelling steps; options and user control permits to enforce bank`s credit risk modelling policy; User control permits to flexibly define roles and activities segregation in credit risk modelling: modeller, validator, system administrator, …; credit risk modelling database stores all developed (unlimited) credit risk models incl. development data sample/history classified by BU, purpose, version, data scientists and other.

- Highest efficiency in credit risk model building & validation: Exhaustive library of credit risk modelling methods incl. required steps and phases; central database storing ‘work in progress’ to allow later continuation of work.

- Credit Risk MachineLearning system guarantees integrity in credit risk model validation: Audit Trail, reporting and modelling history protected with digital hash (block chain technology); permits to validate any report using the digital hash, allowing a strong control over large teams of credit risk modellers; credit risk modelling database keeps all credit risk models together with their development sample, credit risk modelling history (all the steps from raw development sample to final model) and audit trail, permitting a deep and efficient validation.

- Exhaustive reporting by the press of the button: Complete credit risk model report with the push of a bottom outlining all results incl. graphs, plots and descriptive stats; permits a deep and efficient validation, by keeping development sample and credit risk modelling steps in the central database.

- Credit Risk MachineLearning system provides strong model validation features:

– Extensive validation metrics for credit Machine Learning and traditional predictive credit risk models (PD, transition matrices, CCF, LGD, IFRS9, …):

– Full reporting by the push of a button

– Strong model governance: audit trail, user control and other